{kind=link}

Here’s What Every Homeowner Needs to Know

If you’ve recently received a foreclosure notice — or you’re falling behind on mortgage payments and afraid one is coming — you’re not alone, and you have more options than you might think. Foreclosure is one of the most stressful things a homeowner can face. The letters from the bank, the legal notices, the fear of losing your home — it can feel completely overwhelming.

But here is the truth: foreclosure is a process, not an instant event. And at every stage of that process, you have choices. Whether you’ve missed one payment or you’re already deep into the foreclosure timeline, there are real, legal options available to you right now — including selling your home for cash fast enough to stop the foreclosure entirely.

This guide is written specifically for Georgia homeowners. We’ll walk you through exactly how the Georgia foreclosure process works, what your legal rights are, and every option available to you. You can also visit our dedicated avoiding foreclosure in Georgia page for an overview of your options, or read on for the full guide.

Georgia House Buyers LLC has been helping Macon, Warner Robins, and Middle Georgia homeowners sell fast since 2018. If you’re facing foreclosure, call us today at +1 (478) 739-3968 or get a free cash offer at georgiahousebuyers.com — we can often close in as little as 10 days.

What Do You Have To Lose? Get Started Now…

WE BUY HOUSES IN ANY CONDITION in Georgia. There are no commissions or fees and no obligation whatsoever. Start below by giving us a bit of information about your property or call +1 (478) 739-3968…

What Is Foreclosure? A Plain-English Explanation

Foreclosure is the legal process a mortgage lender uses to take back a property when the homeowner stops making payments. When you took out your mortgage, you pledged your home as collateral — meaning if you defaulted, the lender had the legal right to reclaim the property and sell it to recover their losses.

In Georgia, foreclosure is primarily a non-judicial process, which means the lender does NOT have to go through the court system to foreclose on your home. This is important — and alarming — because it means the process can move faster in Georgia than in many other states.

Many homeowners don’t realize how quickly things can escalate. By the time you’re receiving certified letters and legal notices, you may have less time than you think. Understanding the exact timeline is your first step toward protecting yourself.

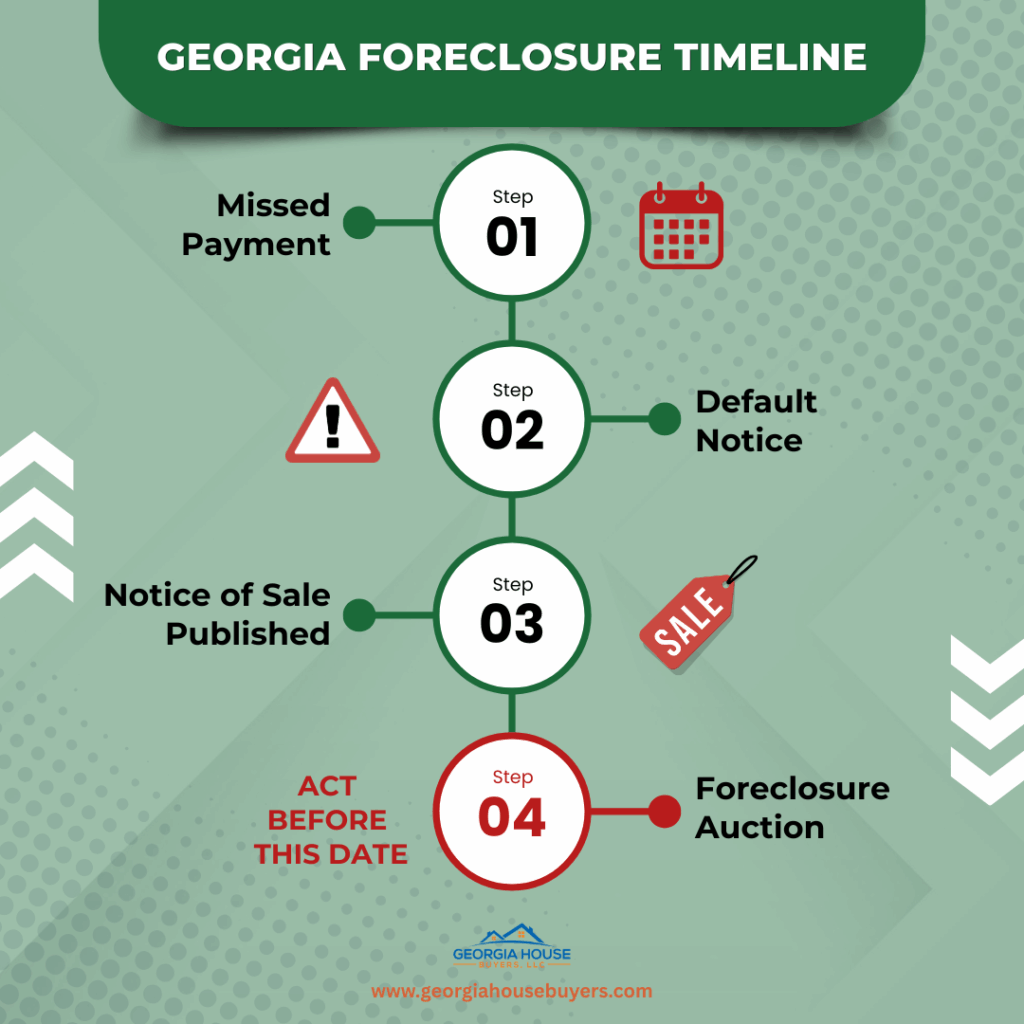

The Georgia Foreclosure Timeline: Step by Step

Here is exactly what the foreclosure process looks like in Georgia, from the first missed payment to the final sale. You can also look up active foreclosure records through the Georgia Courts system for your specific county.

| Stage | Timeframe | What Happens |

| Missed Payment | Day 1–30 | You miss a payment. Late fees begin. The lender may call or send reminder notices. |

| Default Notice | Day 30–90 | After 30–90 days of missed payments, lender sends formal notice of default. |

| Loss Mitigation Period | Days 30–120 | Federal law requires lenders to explore options with you before proceeding. |

| Notice of Sale Published | 21+ days before sale | Georgia law requires the foreclosure sale to be advertised in local newspapers for 4 consecutive weeks. |

| Foreclosure Sale | Typically 60–120 days from default | The property is sold at public auction on the courthouse steps — usually the first Tuesday of the month. |

| Eviction / Redemption | After sale | Georgia has no post-sale redemption period. Once sold, you must vacate. |

How Does Foreclosure Affect Your Credit?

Beyond losing your home, foreclosure can have a devastating impact on your financial future:

- Credit Score Drop: A foreclosure typically causes your credit score to drop by 100–150 points or more.

- 7-Year Credit Record: The foreclosure stays on your credit report for seven years, affecting your ability to get loans, credit cards, apartments, and sometimes employment.

- Deficiency Judgment Risk: In Georgia, if the foreclosure sale doesn’t cover your full loan balance, the lender may sue you for the remaining difference.

- Difficulty Buying Again: After a foreclosure, most conventional mortgage programs require a 7-year waiting period. FHA loans require 3 years.

- Emotional & Mental Health Toll: The stress and uncertainty of foreclosure affects families deeply. Getting ahead of it is better for your wellbeing — not just your finances.

Why Are Georgia Homeowners Facing Foreclosure Right Now?

Foreclosure doesn’t happen because someone is a bad person or a bad homeowner. Life is unpredictable. Here are the most common reasons Middle Georgia homeowners end up in foreclosure:

- Job loss or sudden reduction in income

- Medical bills and unexpected health crises

- Divorce or separation — one income can’t cover the mortgage

- Death of a spouse or co-borrower

- Adjustable-rate mortgage payments that increased beyond what was affordable

- Falling behind during a temporary hardship and never catching up

- Inherited a property with an existing mortgage and unpaid taxes

- Military deployment or relocation causing financial disruption

- Rising property taxes or insurance costs increasing total payments

Whatever the reason, the situation is fixable — but only if you act. Let’s walk through every option available to you.ble to you.

Your Options When Facing Foreclosure in Georgia

You have more choices than the bank wants you to know about. Here’s a complete breakdown of every option available at different stages of the foreclosure process:

Option 1: Contact Your Lender and Request Loss Mitigation

Federal law — specifically the CFPB mortgage servicer rules — requires lenders to review homeowners for loss mitigation options before completing a foreclosure. This means your lender is legally obligated to discuss alternatives with you. You can request:

- Loan Forbearance: A temporary pause or reduction in your monthly payments. You’ll still owe the money, but it gives you breathing room.

- Loan Modification: A permanent change to your loan terms — lowering your interest rate, extending the loan term, or rolling missed payments into the balance.

- Repayment Plan: Spreading your missed payments over several months while continuing to make your regular payment.

- Reinstatement: Paying all missed payments, fees, and penalties in one lump sum to bring the loan current.

Important reality check: Lenders are often slow to respond and difficult to communicate with. These options require paperwork, proof of hardship, and patience — and there is no guarantee of approval.

Option 2: File for Bankruptcy (Chapter 7 or Chapter 13)

Filing for bankruptcy triggers what’s called an automatic stay — which immediately halts all collection actions, including foreclosure proceedings. This can buy you valuable time.

- Chapter 13 Bankruptcy: Allows you to restructure your debt and create a 3–5 year repayment plan. You may be able to keep your home and catch up on missed payments over time.

- Chapter 7 Bankruptcy: Discharges most unsecured debts, but doesn’t stop foreclosure permanently. It can delay the process by several months.

Bankruptcy is a significant legal step with lasting financial consequences. If you cannot afford a private attorney, Georgia Legal Aid offers free legal assistance to qualifying homeowners facing foreclosure. Consult a licensed Georgia bankruptcy attorney before pursuing this option.pursuing this option.

Option 3: Short Sale

A short sale happens when your lender agrees to let you sell the home for less than you owe on the mortgage — and accepts that lower amount as full payment. Short sales:

- Require lender approval, which can take months

- Will still negatively impact your credit, but less severely than a foreclosure

- Usually involve a traditional real estate agent and a lengthy process

- May result in a deficiency waiver — or the lender may still pursue the remaining balance

Short sales can be a viable option if you have time, but they’re slow and uncertain. They’re not the right tool for homeowners who need to move quickly.rs who need to move quickly.

Option 4: Deed in Lieu of Foreclosure

With a deed in lieu, you voluntarily sign your home over to the lender in exchange for being released from the mortgage obligation. This avoids the formal foreclosure process.

- Less damaging to credit than a completed foreclosure

- Lender must agree to the arrangement

- You typically must have no other liens on the property

- You still lose the home, but avoid the legal process and public auction

Option 5: Sell Your Home Fast for Cash — The Georgia House Buyers Solution

This is often the fastest, cleanest, and most financially beneficial option for homeowners in foreclosure — and it’s the one most people don’t know they have until it’s almost too late.

Here’s how it works. You can also learn about our simple 3-step process in full detail on our website:

- You contact Georgia House Buyers LLC — call +1 (478) 739-3968 or fill out the form at georgiahousebuyers.com

- We assess your property and give you a fair, no-obligation cash offer within 48 hours

- You choose the closing date — we can close in as little as 10 days

- The foreclosure is stopped — proceeds from the sale pay off your mortgage

- You walk away with any remaining equity — no fees, no commissions, no repairs

Why selling for cash beats everything else:

Fastest option — can close before the foreclosure sale date

You keep your equity — instead of losing it at auction

No repairs needed — we buy as-is, in any condition

No fees or commissions — you keep more money

Stops the foreclosure — protects your credit from the worst damage Dignified and confidential — no courthouse auction, no public embarrassment

Can You Sell Your House During Foreclosure in Georgia?

Yes — and this surprises many homeowners. As long as the foreclosure sale has not yet happened, you legally own your home and have the right to sell it. Even if you’ve received a Notice of Sale, you can still sell your home up until the moment the auction takes place.

The key is timing. In Georgia, foreclosure sales happen on the first Tuesday of each month. If your auction is scheduled, you have a specific, hard deadline — and a traditional listing simply cannot move fast enough to meet it. Cash buyers like Georgia House Buyers LLC can.

When you sell your home before the foreclosure sale:

- Your mortgage gets paid off: The sale proceeds pay the outstanding loan balance first.

- You keep the equity: Any money left over after paying the mortgage, taxes, and liens goes directly to you.

- Your credit is protected: A voluntary sale hurts your credit far less than a completed foreclosure.

- The legal process stops: No foreclosure on your record. No deficiency judgment risk.

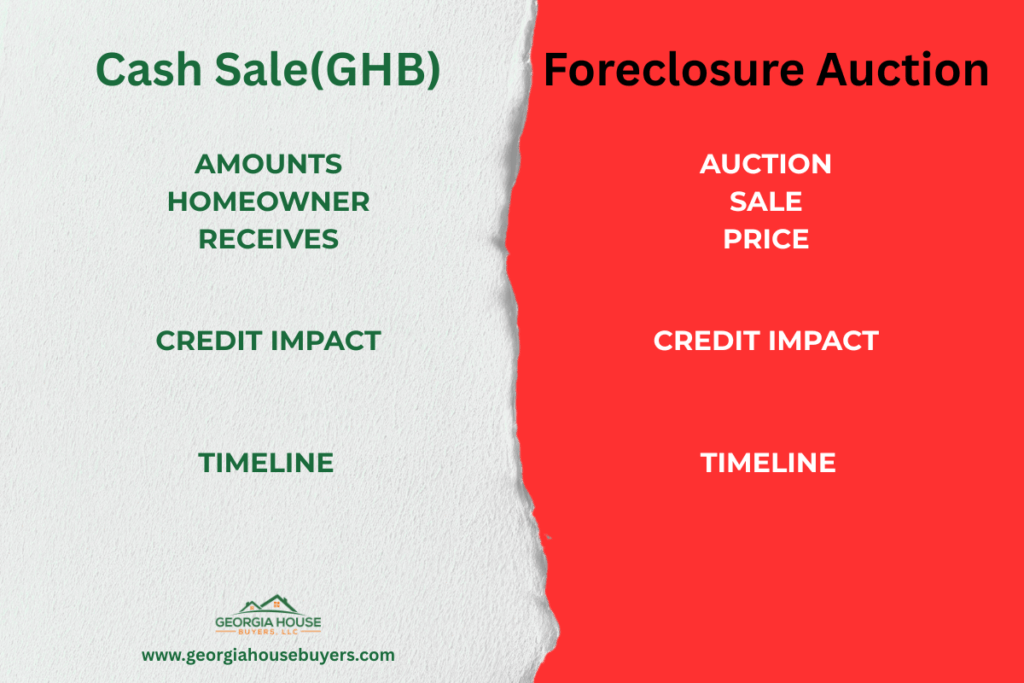

What Happens to Your Equity If You Let the Foreclosure Happen?

This is the part that many homeowners don’t fully understand — and it costs them dearly.

When your home goes to foreclosure auction, the lender is trying to recover what they are owed — not to get you the best price. Foreclosure auctions routinely sell properties for 20–40% below market value. Here’s what that means in practical terms:

| Scenario | Cash Sale (GHB) | Foreclosure Auction |

| Home Market Value | $150,000 | $150,000 |

| Sale Price | $128,000 | $95,000 (typical auction) |

| Mortgage Balance | $87,000 | $87,000 |

| Lender Fees & Costs | $0 | $6,000+ |

| You Receive | $41,000 | $0–$2,000 |

| Credit Impact | Moderate | Severe (7 years) |

| Deficiency Risk | None | Possible |

The math is stark. Homeowners who let the foreclosure proceed often lose tens of thousands of dollars in equity that they could have kept by selling fast to a cash buyer.

Georgia Homeowner Rights During Foreclosure

As a Georgia homeowner facing foreclosure, you have important legal rights. Here’s what you need to know:

Right to HUD Counseling: You’re entitled to free foreclosure counseling through HUD-approved foreclosure avoidance counseling — this is a legitimate free resource that can help you evaluate all your options with an independent advisor.

- Right to Notice: Your lender must send written notice before beginning the foreclosure process. Georgia requires a 30-day notice of intent to foreclose.

Right to Loss Mitigation Review: Under federal mortgage servicer rules, if you submit a complete loss mitigation application more than 37 days before the foreclosure sale, the servicer must review it before proceeding.

- Right to Sell: You can sell your home at any time before the foreclosure auction — and a cash buyer can close fast enough to make that happen.

- Right to Reinstate: In many cases, you can pay all overdue amounts plus fees up until 5 days before the scheduled sale to bring the loan current.

Right to Contest: If your lender violated any laws or procedures, you may be able to challenge the foreclosure in court. Free legal aid for Georgia homeowners is available through Georgia Legal Aid for qualifying individuals.

Foreclosure Scams: What to Watch Out For in Georgia

Sadly, homeowners in foreclosure are prime targets for scams. Here are the most common foreclosure scams in Georgia and how to avoid them:

- Foreclosure Rescue Scams: Someone promises to save your home for an upfront fee — then disappears. Legitimate housing counselors never charge upfront fees.

- Deed Transfer Scams: A company offers to take over your mortgage and let you rent back your home, then transfers the deed and evicts you.

- Fake Short Sale Companies: They claim to negotiate a short sale with your lender but drag the process out while you fall deeper into foreclosure.

- Predatory Cash Buyer Operations: Unethical investors make extremely lowball offers and pressure desperate homeowners to sign quickly.

How to protect yourself: Work only with established, reputable companies. Georgia House Buyers LLC has been operating in Middle Georgia since 2018 with real verified reviews. Read our seller testimonials — real names, real videos, real results. We will never pressure you to sign anything.

How Georgia House Buyers LLC Helps Homeowners Facing Foreclosure

At Georgia House Buyers LLC, we work with homeowners in exactly this situation every week. We understand the stress, the timeline pressures, and the emotional weight of what you’re going through — because we’re a local Middle Georgia company, not a faceless national corporation.

We are licensed Real Estate Agents in the State of Georgia who also act as principals when purchasing investment property. That means full accountability, full transparency, and a team that legally cannot mislead you.

Here’s what working with us looks like:

- One phone call or form submission: Reach us at +1 (478) 739-3968 or gerogiahousebuyers.com. We respond the same day.

- Fair cash offer within 24 hours: We assess your property and make a fair offer — no lowballing, no games. You’re under zero obligation.

- No repairs required: We buy houses in any condition — fire damage, water damage, code violations, bad tenants — it doesn’t matter.

- We pay all closing costs: There are zero fees or commissions. The offer we make is the money you receive.

- Close on your timeline: We can close in as few as 10 days — or give you more time if you need it to move.

- We handle all the paperwork: We work with a local Georgia closing attorney and manage the entire transaction for you.

| What Our Customers Say: “Gerald and Michelle come highly recommended by me. They made the selling of my house super easy and care-free. I was explained the entire process step-by-step upfront, and the information told to me was never changed. I would gladly do business with them again.” — Jasmayne “A wonderful experience! Professional, courteous, fast closing. I highly recommend Michele and Gerald for anyone interested in selling a property.” — Leisa |

Middle Georgia Areas We Serve

Georgia House Buyers LLC buys houses across all of Middle Georgia. We frequently help homeowners facing foreclosure in Macon, Warner Robins, and every surrounding community listed below:

| • Macon • Warner Robins • Milledgeville • Forsyth • Byron • Fort Valley | • Centerville • Kathleen • Bonaire • Gray • Lizella • Juliette | • Bibb County • Houston County • Monroe County • Jones County • Peach County • Baldwin County |

Frequently Asked Questions: Foreclosure in Georgia

How long does foreclosure take in Georgia?

Georgia is a non-judicial foreclosure state, meaning the process can move quickly — typically 60 to 120 days from the first missed payment to the foreclosure auction. The notice of sale must be published for four consecutive weeks in the local newspaper before the sale occurs. You can look up scheduled foreclosure sales through the Georgia Courts system.

Can I stop a foreclosure in Georgia?

Yes — you have several options including loan modification, forbearance, bankruptcy, short sale, and selling to a cash buyer. A cash sale through Georgia House Buyers LLC is often the fastest and most financially sound option. Get a free no-obligation cash offer here.

Will foreclosure affect my credit for 7 years?

Yes. A completed foreclosure remains on your credit report for seven years from the date of the first missed payment. A voluntary sale will still affect your credit but far less severely and for a shorter duration.

Can I sell my house after receiving a foreclosure notice in Georgia?

Absolutely. As long as the foreclosure sale hasn’t taken place, you legally own the property and can sell it. Georgia House Buyers LLC can often close in 10 days. Learn about our process here.

Do I keep any money if my house is foreclosed on?

Only if the auction sale price exceeds your total mortgage balance plus all lender costs — which rarely happens. Most homeowners in foreclosure walk away with nothing. If you sell before the auction, you keep any equity above your mortgage payoff.

Does Georgia House Buyers LLC buy houses with liens?

Yes. We work with homeowners who have tax liens, HOA liens, second mortgages, and other encumbrances. See our full FAQ for home sellers for more detail on how we handle complex title situations.

What if I also have unpaid property taxes?

Unpaid property taxes create a lien on your home that must be resolved at closing, but they do not prevent a sale. We routinely help homeowners resolve tax liens as part of the transaction. You can check your current tax balance through the Bibb County Tax Commissioner.

Steps to Take Right Now If You’re Facing Foreclosure

If you’re reading this because you’re in or near foreclosure, here’s your action plan:

- Know your exact timeline. Find out when your foreclosure auction is scheduled. If you don’t know, contact your lender or check your county’s public foreclosure notices.

- Contact a HUD-approved housing counselor. HUD-approved foreclosure avoidance counseling is free and can help you understand your options with your specific lender.

- Call Georgia House Buyers LLC immediately. +1 (478) 739-3968 — or get your free cash offer online here. We’ll tell you honestly whether a cash sale can work for your situation and timeline. No pressure, no obligation.

- Talk to a Georgia real estate attorney. If you believe your lender has violated any laws or procedures, free legal aid for Georgia homeowners may be able to help you slow or stop the foreclosure.

- Do not ignore the notices. The biggest mistake homeowners make is freezing up and hoping the situation will resolve itself. Every day of inaction costs you options.

Conclusion: You Have Options — But Time Matters

Facing foreclosure is terrifying, but it is not the end of your story. Georgia law gives you time and options — but that window closes fast, and waiting costs you money, your credit, and potentially tens of thousands of dollars in equity.

The homeowners we work with at Georgia House Buyers LLC always say the same thing afterward: they wish they had called sooner. The process is simple, fast, and honest. We’ll give you a fair offer, let you choose your closing date, and get you out from under the burden — with money in your pocket.

Don’t let the bank make that decision for you at a courthouse auction. Get your free cash offer today or call +1 (478) 739-3968. There is never any obligation, and we can close in as little as 10 days.

Ready to Stop the Foreclosure? Contact Georgia House Buyers LLC Today.

Call: +1 (478) 739-3968 | georgiahousebuyers.com

No fees. No commissions. No repairs. Close in as little as 10 days.

Serving Macon, Warner Robins, and all of Middle Georgia since 2018.